When discussing sustainability, terms like “Scope 1, Scope 2, and Scope 3” frequently come up. These concepts are essential for understanding and managing the climate impact of companies, projects, and organizations. Let’s explore what these scopes mean and why they are crucial.

Direct vs. Indirect Emissions

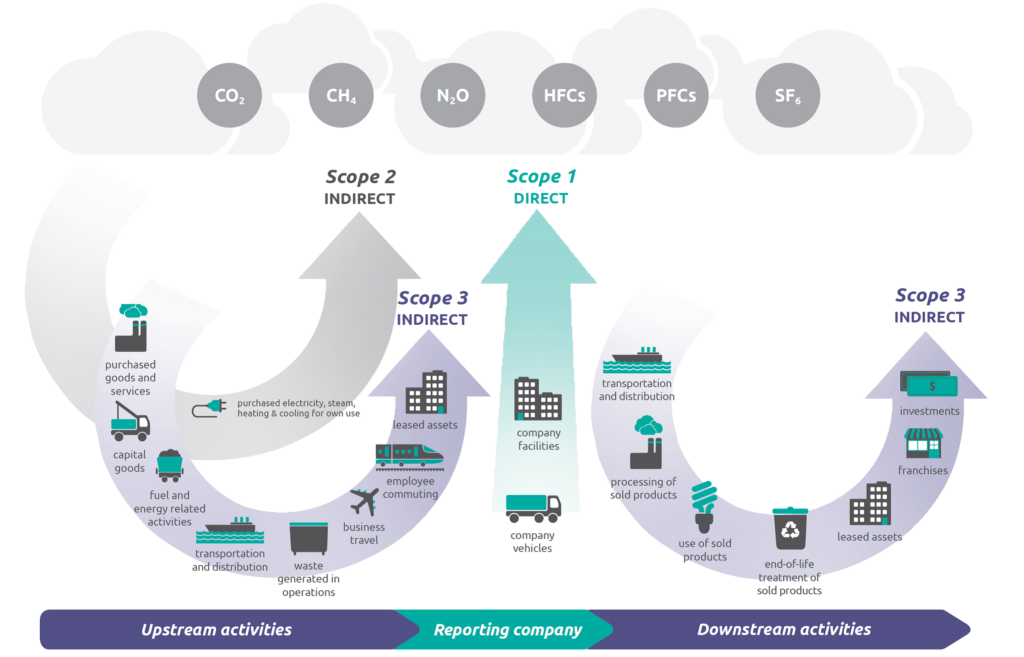

According to the GHG Protocol methodology, greenhouse gas (GHG) emissions related to an organization’s activities are divided into direct and indirect emissions. Scope 1 emissions (also known as direct emissions) refer to emissions from sources and processes directly controlled by the company. For example, this could be energy production from burning biomass on-site. Scope 2 and Scope 3 emissions are indirect, meaning they result from the company’s activities but are not directly controlled by the company.

Why are Emissions Categorized Into Three Scopes?

To effectively reduce emissions, it’s crucial to understand and measure where they come from. The three scopes help distinguish different types of emissions generated by a company’s activities and its broader value chain.

Why are they called “scopes” instead of “categories” or “types”? The terminology comes from the GHG Protocol, the world’s most widely used greenhouse gas accounting standard.

The GHG Protocol states: “A complete [greenhouse gas] emissions inventory – encompassing Scope 1, Scope 2, and Scope 3 emissions – allows companies to understand their entire value chain emissions and focus on the most significant reduction opportunities.”

This three-scope structure provides a clear and methodical framework for assessing an organization’s GHG footprint. Differentiating between emission sources creates a solid foundation for data collection, identifying high-impact activities, setting goals, and developing improvement measures. A scope-based approach also simplifies reporting on GHG footprint assessment results and helps avoid double-counting across various business areas.

Scope 1: Direct Emissions

As mentioned earlier, Scope 1 covers direct emissions from sources controlled or owned by the company. These include on-site energy production (such as heat energy generated by burning biomass), mechanical or chemical processes, and emissions from the company’s vehicle fleet.

Typically, the largest Scope 1 emissions occur in the energy and manufacturing sectors. These sectors are often associated with significant direct emissions, frequently linked to fossil fuel combustion for energy production (e.g., power plants, refineries) and industrial processes (e.g., steel and cement production). These processes directly emit large quantities of greenhouse gases, such as carbon dioxide (CO2) and methane (CH4).

Scope 2: Indirect Emissions

Scope 2 emissions are related to the energy purchased and consumed by the company, such as electricity, heat, cooling, and steam. If the purchased energy comes from non-renewable sources (e.g., oil shale), Scope 2 emissions can be substantial, especially for offices, retail chains, large manufacturing plants, and data centers that rely heavily on electricity for lighting, heating, cooling, and production processes.

Scope 3: Indirect Emissions Across the Value Chain

Scope 3 encompasses all other indirect emissions that do not stem from assets owned or controlled by the company but are associated with upstream and downstream activities within the value chain. This includes emissions from purchasing, using, and disposing of products from suppliers. Scope 3 emissions cover all sources outside the boundaries of Scope 1 and Scope 2.

Typically, the largest Scope 3 emissions occur in sectors driven by manufacturing and supply chains, such as the automotive, electronics, and apparel industries. These sectors generate significant emissions throughout the production chain, including raw material extraction, component manufacturing, logistics, supplier activities, product use, and waste management. Because Scope 3 covers the entire value chain’s indirect emissions, they can be significantly larger than Scope 1 and Scope 2 emissions and may constitute the majority of a company’s carbon footprint. Often, Scope 3 categories are the most challenging part of a GHG inventory.

What are Upstream and Downstream Emissions in Scope 3?

Scope 3 emissions are further divided into upstream and downstream activities.

Upstream emissions encompass the indirect GHG emissions generated during the production of goods and services procured or supplied by the organization. These emissions occur from raw material extraction to product receipt by the company, also known as the “cradle-to-gate” approach.

Downstream emissions occur after the final products leave the company and include GHG emissions associated with product transportation, sales, use, and disposal at the end of their life cycle, also known as the “gate-to-grave” approach.

Carbon Dioxide Equivalent vs. Greenhouse Gases

Here, we also clarify the concepts of greenhouse gases (GHGs) and carbon dioxide equivalent (CO2e).

When assessing the GHG footprint, it’s essential to define which greenhouse gases will be evaluated. Carbon dioxide (CO2) is perhaps the most well-known GHG, but there are others. The GHG Protocol and other international guidelines stipulate that a GHG footprint assessment must include at least seven major GHGs:

- Carbon dioxide (CO2)

- Methane (CH4)

- Nitrous oxide (N2O)

- Hydrofluorocarbons (HFCs)

- Perfluorocarbons (PFCs)

- Sulfur hexafluoride (SF6)

- Nitrogen trifluoride (NF3)

CO2 equivalent (CO2e) is a unit of measurement used to express the impact of different GHGs on the climate in a standardized and comparable way. Each greenhouse gas has a different global warming potential (GWP), which determines how much heat it can trap in the atmosphere relative to CO2 over a specific time period, typically 100 years. For example, methane (CH4) has a GWP approximately 28-34 times greater than CO2, meaning one ton of methane has the same climate impact as 28-34 tons of CO2. Nitrous oxide (N2O) has an even higher GWP, about 298 times greater than CO2.

When calculating CO2 equivalents, the quantity of each greenhouse gas emitted is multiplied by its GWP to express its impact relative to CO2. For instance, if a company emits one ton of methane, this is considered equivalent to 28-34 tons of CO2. This approach allows the various impacts of different greenhouse gases to be consolidated into a single value, simplifying their assessment and management in the context of climate change. Therefore, when discussing a company’s carbon footprint, it actually encompasses the impact of all greenhouse gases, expressed in CO2 equivalents.

If you want more information or help with the calculation of your organization’s GHG, leave us your contact via the form below!

"*" indicates required fields